In today's Pulse article, Kelvin Davidson analyses the current mortgage lending environment in New Zealand.

Given the scrapping of first home grants (deposit assistance) and also the strong indication from the latest Monetary Policy Statement that mortgage rates are set to be ‘higher for longer’, there’s bound to be a continued focus on the general property lending environment and, in particular, how easy or hard it is to access lower deposit finance. Let’s take a look at where the current landscape stands right now.

1.The slow and steady recovery in gross new lending activity continued in April.

Across house purchases, bank switches, and loan top-ups (equity withdrawal), total lending was $5.9bn last month, up by $1.6bn from April 2023, and the eighth rise in the past nine months, albeit from a low starting point.

2. Interest-only lending is ‘under control’.

Recently around 15% of lending to owner-occupiers has been interest-only, and 30-35% for investors. Going back to 2015-16, those figures were closer to 35% and 55% respectively. In some ways, it would appear that interest-only lending has recently become more of a useful fallback position rather than the primary go-to choice.

3. Average loan sizes in April were around $545,000 for investors and $555,000 for first home buyers (FHBs).

Based on the median price paid by FHBs in April of $700,000 from CoreLogic data, the implication is that a typical deposit is currently in the vicinity of $145,000, or pretty close to the 20% mark.

4. But many FHBs continue to access the market with <20% deposits.

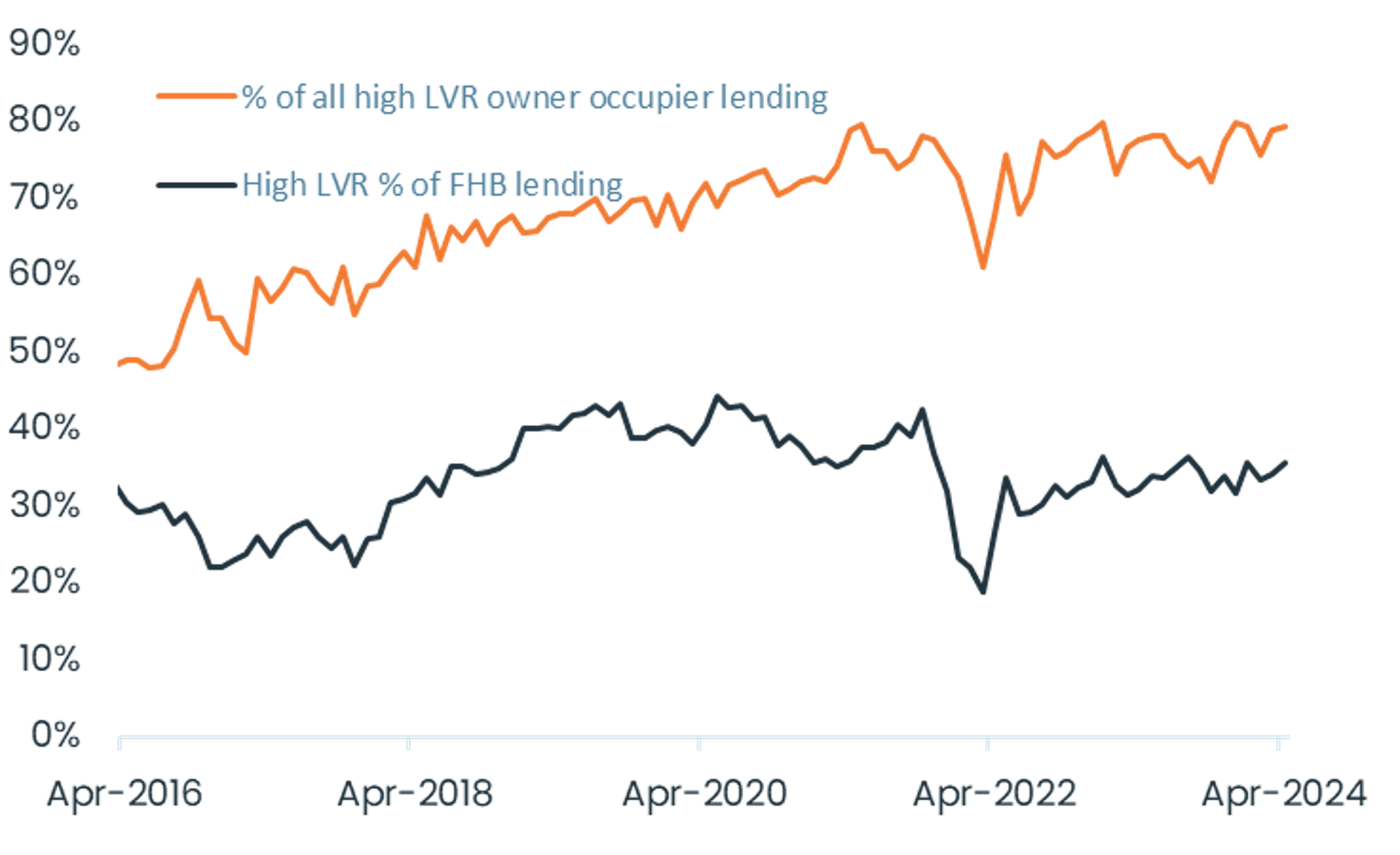

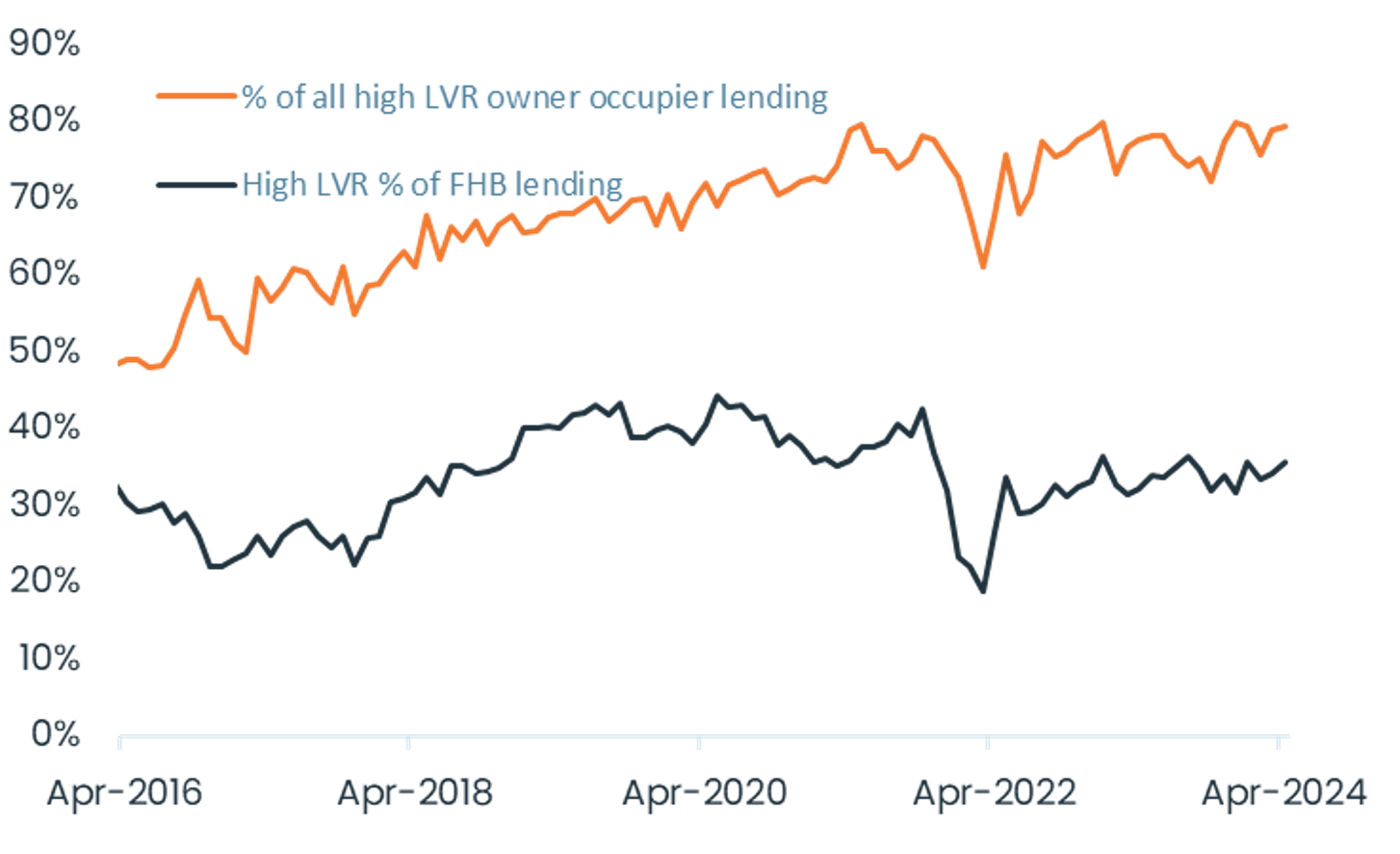

Compared to the 15% speed limit allowance for banks to lend to owner-occupiers with less than a 20% deposit, only 9% in April actually went out in that bracket (although banks’ tendency to keep a 5% buffer, means the ‘real’ speed limit is probably 10%). In turn, as Figure 1 below shows, within that 9%, about four-fifths (orange line) actually went to FHBs, and put another way, around one-third (blue line) of FHBs have recently been getting mortgages with less than a 20% deposit. This has been a key support for FHBs’ ability to buy.

5. The likely loosening of the LVR rules should continue to assist FHBs.

Given that the low deposit lending speed limit is likely to rise from 15% to 20% over the next few months, FHBs should continue to have reasonable access to the market, provided of course that they can meet the serviceability testing requirements.

Figure 1. High LVR first home buyer lending (Source: RBNZ)

6. Investors stand to benefit from looser LVRs too.

Soon five percent of new lending is set to be allowed at less than a 30% deposit, an easing from the current 35% deposit requirement. At present, essentially no investor lending to purchase existing properties is taking place in the 30-35% deposit bracket. Clearly, the change in the rules would open this up, and also allow existing investors to free up some more equity from the rest of their portfolio too. Of course, low rental yields and high mortgage rates (hence large cashflow top-ups) will remain key challenges for investors looking at purchasing more properties for a while.

7. Debt to income limits are a big deal.

Given that mortgage rates remain high, the size of loans being approved lately has naturally been lower than before in relation to borrowers’ income – less than 10% of lending was done at a high DTI for both first home buyers and investors over the first few months of 2024. But even though the likely near-term introduction of formal caps on DTIs might not do much straightaway, make no mistake, the new rules will mark a big landscape shift as mortgage rates decline – primarily by slowing down the rate at which property investors can grow a portfolio, especially in more expensive areas.

8. The process to reprice existing loans to current mortgage rates isn’t finished just yet.

In Figure 2, the latest data shows 60% of existing mortgages (by value) are fixed but due to reprice to a new mortgage rate within the next 12 months. Now, some of those loans won’t see much of a change. But others could easily see their mortgage rate go up by 0.5% to 1%, maybe more – indeed the Reserve Bank estimated in their latest Financial Stability Report that around 20% of borrowers still have debt at a rate 5% or less.

9. Job losses are a clear risk to the smooth repricing process so far.

Not only are some borrowers yet to hit market rates, but the labour market is now softening too, with some job cuts coming through. That will tend to drive more repayment stress, non-performing loans, and possibly mortgagee sales. But the context is also important; the Reserve Bank is still projecting a higher unemployment rate mostly due to a bigger labour force (not mass job losses), and those measures of stress in the housing market are starting from very low levels.

10. There are many people with a lot of housing equity.

Finally, it’s worth remembering that many people don’t have a mortgage and there’s a big equity buffer out there. CoreLogic estimates show the housing stock is currently worth $1.63trn, while RBNZ data shows a mortgage stock of $358bn, implying an overall LVR of only 22% or so.

Figure 2. Breakdown of existing mortgages by time to next repricing (Source: RBNZ)

Meet Kelvin Davidson

Chief Economist

Kelvin joined CoreLogic in March 2018 as Senior Research Analyst, before moving into his current role of Chief Economist. He brings with him a wealth of experience, having spent 15 years working largely in private sector economic consultancies in both New Zealand and the UK.

Full profile