CoreLogic's House Price Index (HPI), which is the most robust measure of property value change in the market, shows the NZ property market has weakened further as credit tightens and interest rates increase.

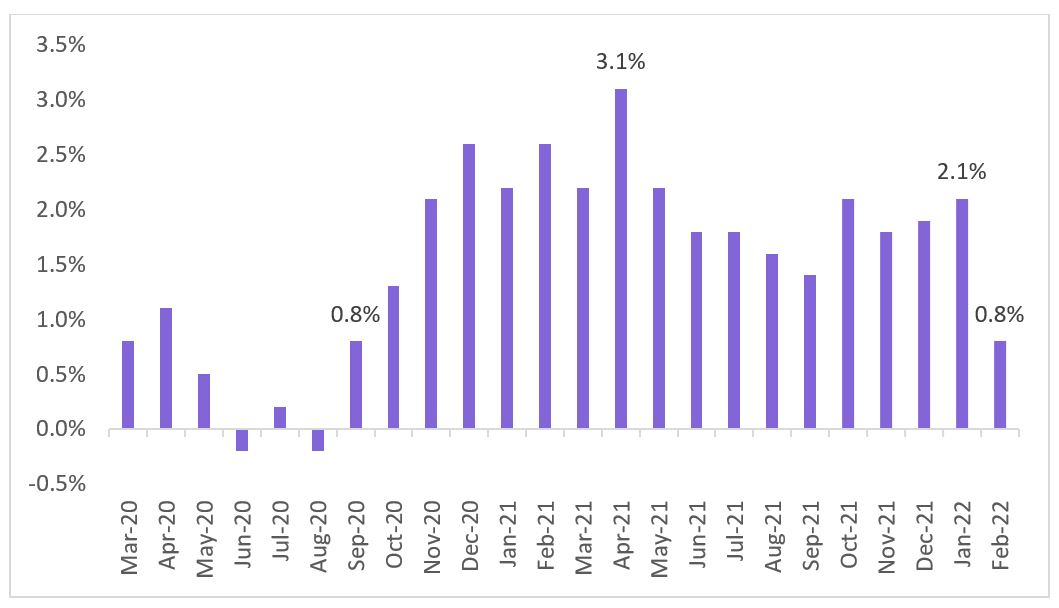

The national measure of housing prices was 0.8% higher in February, a sharp drop from the January reading of 2.1% and down from the cyclical peak rate of 3.1% growth in April 2021.

Given the index incorporates sales data from the past three months, February's positive reading can be attributed to stronger sales evidence prior to Christmas. CoreLogic analysis of very recent sales, including unconfirmed sales, shows sentiment is changing rapidly, with vendors unable to achieve the prices of 2021.

Recently published lending data for January from the Reserve Bank shows a significant drop in mortgage activity, adding additional weight to the worsening housing outlook. This trend is likely to persist, as stretched affordability and improved choice for buyers compounds the impact of tighter, more expensive lending.

The lending data also showed first home buyers are being hit extra hard by recent changes in the credit environment, from the reduced allowance for low deposit lending and tighter income/expense checking under the Credit Contracts and Consumer Finance Act (CCCFA).

CoreLogic NZ Head of Research Nick Goodall said: "Our expectation is the HPI will dip further over the coming months as continued rate hikes and tighter credit controls weigh on market conditions. The significant drop in the monthly rate of growth from January to February indicates a clear change in trend.

"Regional differences will also start to appear, as local economies, recent first home buyers and property investors all react differently to the changing environment.”

It's the lowest rate of growth since September 2020, which marked the start of New Zealand's exceptional 18-month growth phase. At that time, the strictest of the initial national lockdowns had been eased, uncertainty had dramatically reduced and the Government and Reserve Bank fiscal and monetary support was directing money into assets.

CoreLogic House Price Index – National monthly rate of change (since the pandemic hit)

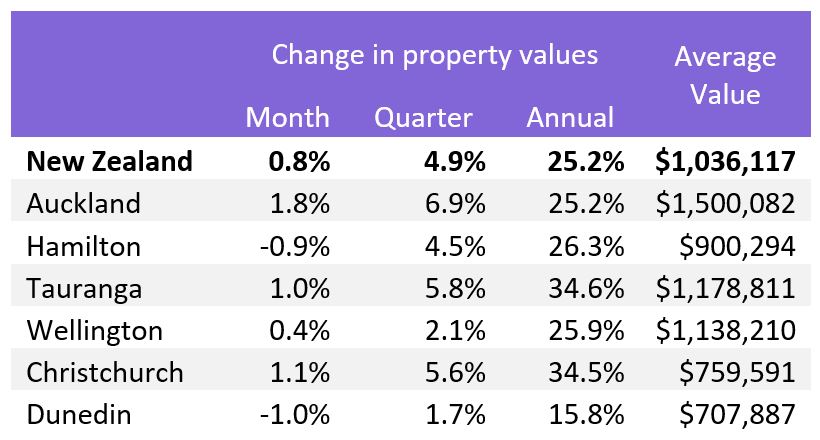

CoreLogic House Price Index - National and Main Centres

Out of our six main centres, Dunedin (-1.0% monthly) and Hamilton (-0.9%) showed the greatest signs of weakness over February, while growth in Wellington has moderated significantly (+0.4%).

In Auckland, where the average property is now worth more than $1.5million, values are showing more resilience recording a growth rate of 1.8% for February. Beneath the surface however, the more expensive markets of North Shore ($1.67million and 0.0%) and Auckland City isthmus ($1.72million and 1.0%), along with the more ‘rural' Rodney area ($1.39million and -0.3%) have shown visible signs that growth has slowed.

Property values in both Christchurch (1.1%) and Tauranga (1.0%) have also retained some momentum from the end of 2021, however growth has trended lower over the past few months.

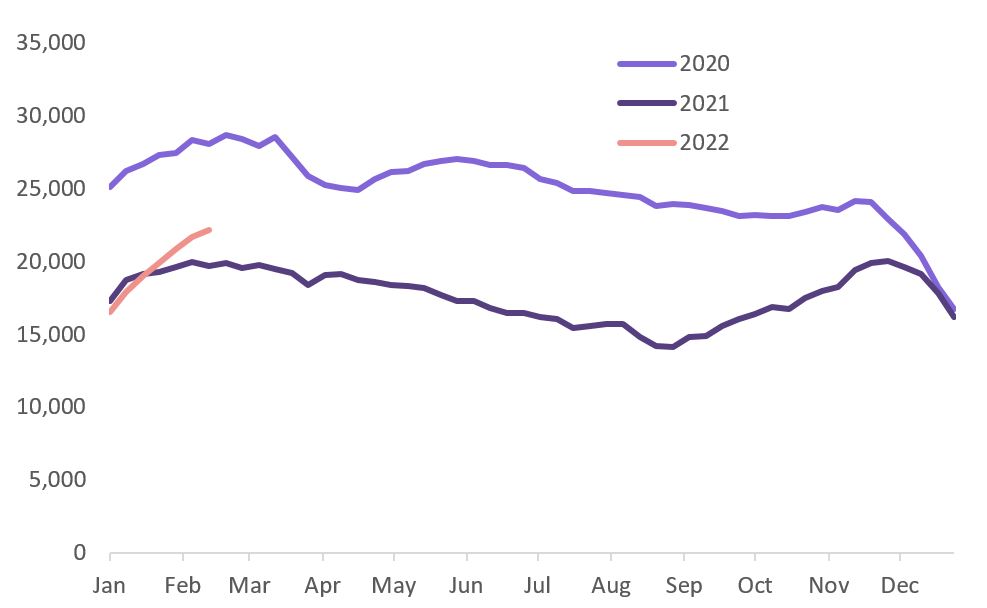

Changes in advertised stock levels are also likely to be influencing recent price changes. Nationally total listings are greater than at any time in the last year, while in some parts of the country, such as Upper Hutt, the total stock levels have increased three-fold in the past year.

Total listings for sale

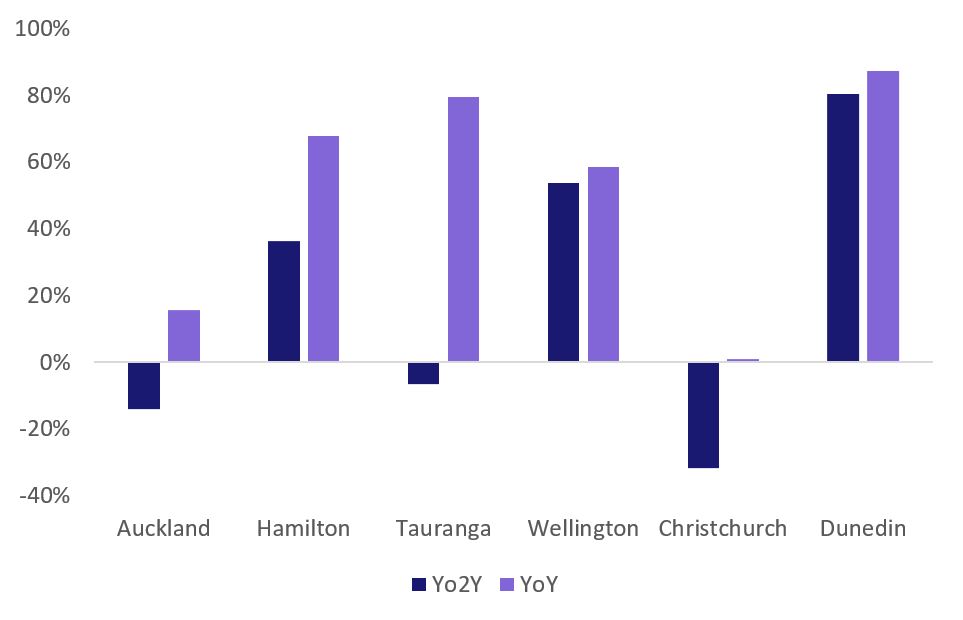

Total listings year-on-year change – Main Centres

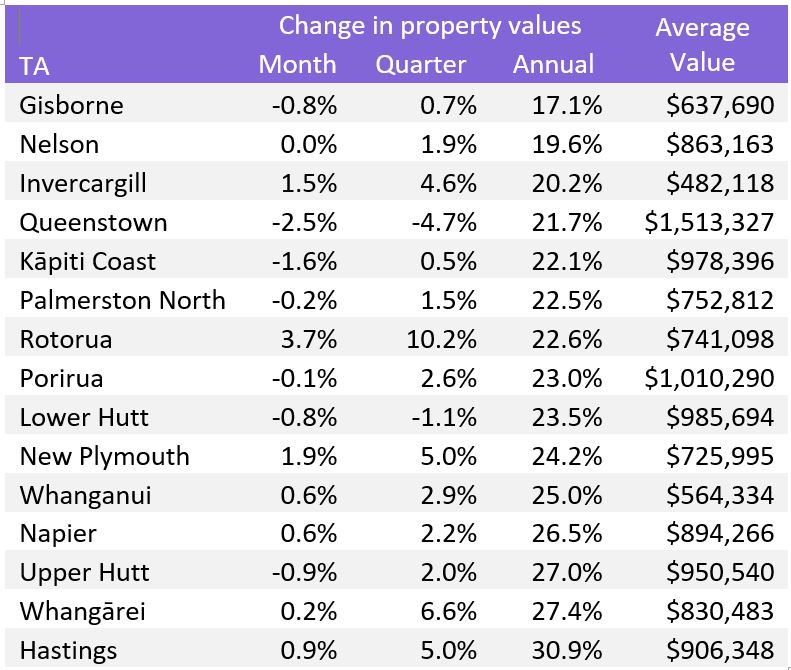

Provincial Centres ordered by annual growth

The weakening trend in property growth is evident across most of our other main urban areas also.

Rotorua is the one area where property value growth accelerated – increasing 3.7% over the month, taking the annual rate of growth to 22.6%. All other areas saw a reduction in the quarterly rate of growth compared to January.

Queenstown (-4.7%) and Lower Hutt (-1.1%) saw values decline over the longer three-month period, while Kāpiti Coast, Upper Hutt, Gisborne, Palmerston North and Porirua experienced a decline in average property values over the month.

Weakness appears to be impacting the southern and eastern cities of the North Island first – locations where the latest upswing in values has been most significant.

Looking ahead, the Government's review of the December 1 changes and implementation of the CCCFA may see credit conditions loosen in the future, but for now, the outcome of the review remains uncertain, entrenching the current choking of property demand.

The RBNZ's consultation period for the potential introduction of debt-to-income (DTI) restrictions has also closed. Given the widespread slowdown occurring across the market it is unlikely any restrictions will be implemented this year, however it will remain a useful tool for the Bank to call upon if needed.

Recent changes to self-isolation and managed isolation and quarantine (MIQ) requirements will be welcome news for many ex-pat Kiwi wanting to return home, either temporarily or permanently. This could add to property demand levels, however there is likely to be an outflow of Kiwis too, as many take delayed overseas trips or relocate to greener pastures, often to Australia.

Tracking net migration figures will be important in relation to the property market, however we don't expect to see the pre-pandemic record highs (>94,000) any time soon. In the short-term credit conditions and affordability will have a greater impact on the housing marketing than migration figures.

On a global stage, Russia's invasion of Ukraine adds another layer of uncertainty, among ongoing Covid complications. Any direct short-term impact to Aotearoa property prices is likely to be muted, not-least because property is a relatively illiquid asset, however with inflation expectations increasing and timelines to resolution impossible to predict, there are potential downside risks to property values.

The Reserve Bank is facing a tricky balancing act at present, with inflation rising (requiring a higher official cash rate) and signs of weakness emerging in the real economy, such as slumping business confidence, the housing market outlook is softening.DOWNLOAD THE FEBRUARY HPI DATA

Enquire about the CoreLogic House Price Index, request a copy of the latest data or subscribe to future updates here.

Meet Nick Goodall

Head of Research

Nick is an ace with numbers, and he has a knack for transforming facts and figures into compelling stories to inform a wide range of audiences. As our Head of Research, Nick is at the forefront of the latest trends driving the NZ property market.

Full profile